Macroeconomic and Geopolitical Evaluation of U.S. Sovereign Debt Consolidation: Universal Tariffs Versus a Hypothetical Allied 1 Trillion annual Security Grant

Google Gemini Advanced 3.1 Pro Report based on my proposal to give America a 1 trillion Grant for 10 to 20 years for Historical Military and Financial Protection.

An earlier report about two World Problems was this one:

So now I asked Gemini to look at the same problem but now only Hypothetical.

The Hypothetical Report

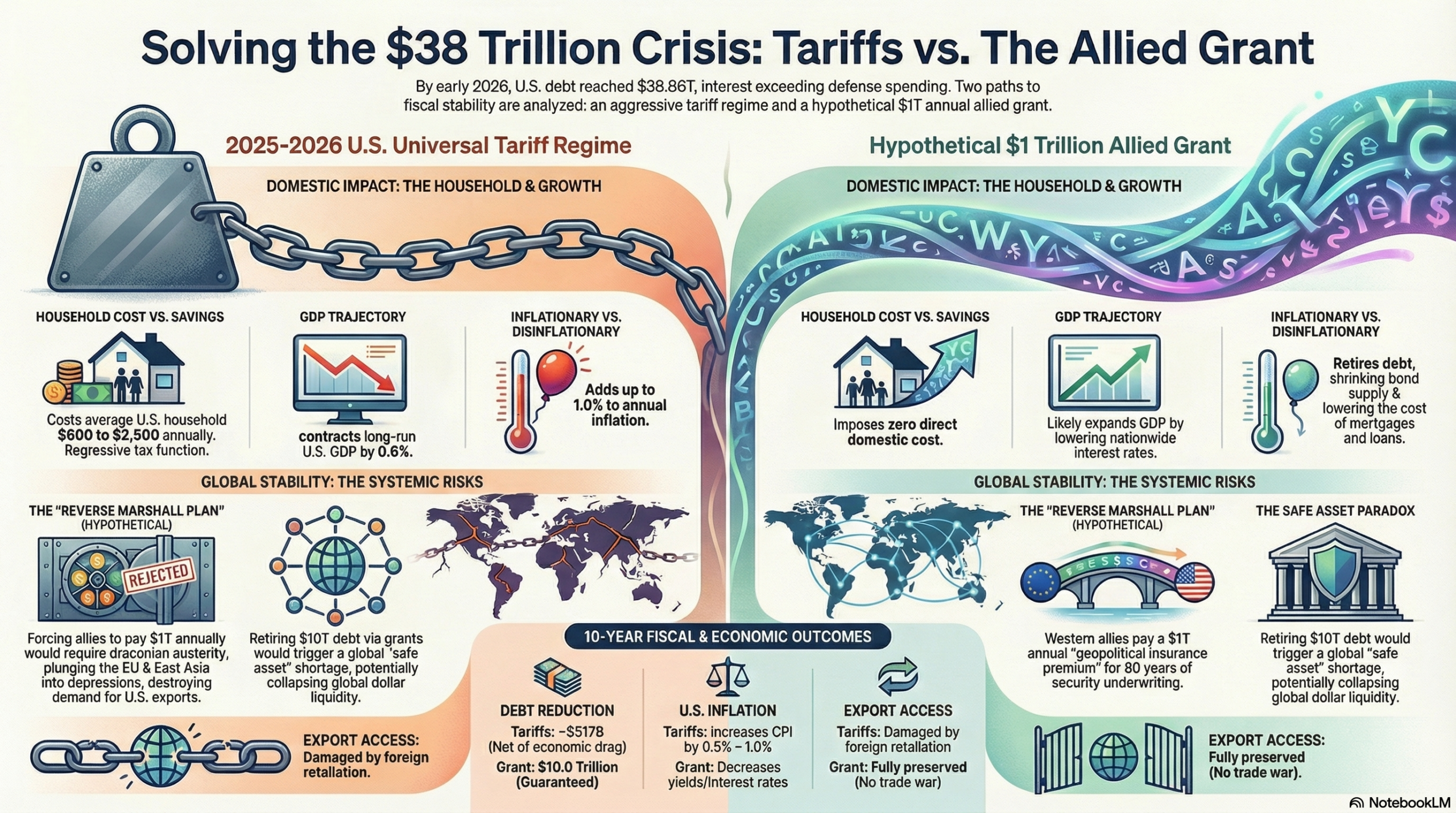

The contemporary global economic order is currently navigating an unprecedented structural realignment, driven by the unsustainable trajectory of sovereign debt within the world’s largest economy. As of early 2026, the gross national debt of the United States has breached the $38.86 trillion threshold, representing approximately 122 percent of the nation’s Gross Domestic Product.1 This severe fiscal imbalance has fundamentally altered the macroeconomic landscape, transitioning the United States from an era of expansionary fiscal dominance into a period defined by the crippling realities of debt servicing. Annual net interest payments on this debt are projected to exceed $1 trillion in fiscal year 2026, consuming nearly 18.6 percent of all federal revenue and officially surpassing the entirety of the U.S. national defense budget.4

To address this paralyzing fiscal burden and offset domestic tax cuts, the U.S. administration deployed a highly aggressive, protectionist trade agenda throughout 2025 and 2026. This strategy was characterized by the implementation of near-universal tariffs ranging from 10 percent to 20 percent on global imports, alongside punitive tariffs exceeding 60 percent on geopolitical rivals, utilizing executive authorities such as Section 122 and the International Emergency Economic Powers Act.8 While ostensibly designed to raise trillions in federal revenue and protect domestic manufacturing, the macroeconomic reality of this tariff disruption has been severe. The policies have triggered retaliatory trade wars, disrupted global supply chains, and functioned as a highly regressive consumption tax on American households, exacerbating inflationary pressures without fundamentally stabilizing the long-term debt trajectory.11

Given the vast domestic friction and international alienation caused by the 2025–2026 tariff regime, an alternative theoretical paradigm warrants rigorous macroeconomic analysis. This paradigm involves a hypothetical scenario wherein, rather than disrupting global trade through unilateral tariffs, the United States is provided a $1 trillion annual non-repayable grant by a coalition of advanced Western allies for a period of ten years. Grounded in the principles of Hegemonic Stability Theory, this proposal suggests that allied nations—who have historically relied heavily on the U.S. security umbrella, nuclear deterrence, and naval protection of global sea lanes—should retroactively compensate the United States for underwriting the historical stability of the global order.15

While institutional realities, such as the mandate limitations of the International Monetary Fund and the structural dependencies of global dollar liquidity, render this direct grant mechanism functionally impossible to orchestrate in the current political world order 15, analyzing it as a pure macroeconomic counterfactual provides profound insights. This report delivers an exhaustive comparative analysis of these two debt-reduction pathways. By evaluating the real-world consequences of the recent tariff disruptions against the theoretical outcomes of a massive, coordinated external capital transfer, this analysis determines whether the hypothetical grant would have provided a more economically efficient, consumer-friendly, and cheaper method for rectifying the $38.86 trillion U.S. debt crisis.

The Anatomy and Trajectory of the $38 Trillion U.S. Sovereign Debt Crisis

Understanding the relative efficacy of universal tariffs versus direct external grants requires a precise diagnostic of the U.S. sovereign debt architecture. The accumulation of $38.86 trillion in gross national debt is not solely the result of recent fiscal policy, but rather the culmination of decades of structural deficits, compounding interest rates, and massive expenditures related to global security and domestic entitlement programs.2

The velocity of this debt accumulation is historically anomalous. It required over two centuries for the United States to accumulate its first trillion dollars in debt; however, the transition from $37 trillion to $38 trillion occurred over a mere matter of months in late 2025, with the debt expanding at an average rate of $7.23 billion per day, or approximately $83,721 every single second.3 The burden of this debt is heavily concentrated in its servicing costs. As the Federal Reserve shifted away from a zero-interest-rate policy to combat post-pandemic inflation, the average interest rate on total marketable U.S. debt rose to 3.355 percent by February 2026, a drastic increase from the 1.512 percent average observed just five years prior.2

| Macroeconomic Debt Metric | Current Status (March 2026) | Projected Status (2036) | Systemic Implication |

| Gross National Debt | $38.86 Trillion | > $63.8 Trillion | Unprecedented sovereign burden constraining future federal fiscal policy and crisis response. |

| Debt-to-GDP Ratio (Publicly Held) | ~101% | 120% | Highest ratio since the post-WWII era, severely limiting macroeconomic flexibility. |

| Annual Interest Expense | > $1.0 Trillion | > $2.1 Trillion | Crowds out national defense spending, infrastructure, and essential domestic investments. |

| Interest as % of Federal Revenue | 18.6% | 25.8% | Narrows the fiscal space available for all non-mandatory government functions. |

| Unfunded Liabilities (75-Year) | $79.6 Trillion | Expanding | Driven almost entirely by mandatory entitlement obligations, specifically Medicare and Social Security. |

Table 1: The Anatomy and Trajectory of U.S. Sovereign Debt and Servicing Costs. 2

The underlying drivers of this paralyzing debt are fundamentally dual-natured. Domestically, the U.S. faces an $88.4 trillion unfunded liability gap driven almost entirely by mandatory entitlement programs such as Social Security and Medicare, which are projected to face trust fund depletion within the next decade if left unaddressed.18 The Congressional Budget Office estimates that by 2036, the combination of interest costs, Social Security, Medicare, and Medicaid will consume 100 percent of all federal revenues, leaving no capital for discretionary spending.20

Internationally, the debt reflects the multi-generational cost of maintaining U.S. global hegemony. Since the end of World War II, the United States has functioned as the primary provider of global security, a role that has required immense deficit spending. The U.S. military apparatus, particularly the U.S. Navy, single-handedly secures the global maritime commons, protecting the sea lanes through which 90 percent of global trade travels.21 This maritime security allows for the uninterrupted flow of critical minerals, energy resources, and manufactured goods that form the backbone of the global economy.24 Furthermore, U.S. military interventions, counter-terrorism operations, and overseas basing strategies have accrued immense long-term budgetary costs. For example, the post-9/11 military engagements in the broader Middle East have incurred estimated total budgetary costs ranging from $9.65 trillion to $12.07 trillion when factoring in future veterans’ care and interest on war borrowing.26

For decades, advanced economies in Europe and East Asia were able to drastically limit their own defense expenditures because their territorial sovereignty and export routes were guaranteed by the American military umbrella.15 In NATO, for instance, many of the wealthiest European members ignored the alliance’s 2 percent of GDP spending target for nearly a decade following the 2014 annexation of Crimea. This resulted in European NATO members collectively underfunding their own defense by an estimated $827.91 billion since 2014—a shortfall nearly equal to the entire annual U.S. defense budget.28 Consequently, a significant portion of the U.S. national debt can be analytically categorized as an indirect subsidy provided by the American taxpayer to allied nations, enabling the “Western World” to divert domestic capital toward robust social welfare programs, healthcare systems, and infrastructure development.15 It is the recognition of this historical asymmetry that fuels both the populist demand for punitive universal tariffs and the theoretical justification for a massive, retroactive allied grant.

Quantifying the Value of Historical Protection and the Justification for Allied Compensation

Before comparing the mechanisms of debt reduction, it is essential to validate the premise underlying the hypothetical $1 trillion annual grant: the assertion that the “Western World” has received immense financial and security value from the United States that justifies such a massive capital transfer. The economic value of the U.S. security umbrella, while difficult to precisely monetize on a balance sheet, is undeniably vast and foundational to the prosperity of allied nations.

The most glaring metric of this value transfer is the disparity in global defense spending. In 2024 and 2025, the United States earmarked approximately $850 billion to $916 billion annually for national defense, representing over 3.3 percent of its GDP.29 By contrast, prior to the outbreak of the war in Ukraine, many NATO allies spent barely 1.5 percent of their GDP on defense, relying on the U.S. extended deterrence—including the U.S. nuclear umbrella—to ward off aggression from geopolitical rivals like Russia and China.28 The RAND Corporation and the Center for Strategic and International Studies have extensively documented how this burden-sharing asymmetry allowed nations like Germany and Japan to prioritize export-led economic growth and domestic prosperity while the U.S. absorbed the frictional costs of maintaining international order.34 If the United States were not in NATO, or if it were to withdraw its extended deterrence from East Asia, allied nations would be forced to increase their own defense budgets by hundreds of billions of dollars annually to fill the security vacuum.32

Beyond terrestrial defense, the economic value of U.S. sea lane protection is astronomical. Over 80 percent of global trade by volume, and 70 percent by value, is transported by sea, relying on a network of international straits and canals.25 The U.S. Navy acts as the ultimate guarantor of this maritime transit, conducting counterpiracy operations, ensuring freedom of navigation, and protecting the undersea cables that carry 97 percent of global data and financial transactions.21 Disruptions to these maritime routes, as witnessed during localized conflicts in the Red Sea or the Malacca Strait, pose direct threats to international food security, energy supplies, and economic stability.25 Because the U.S. owns virtually no commercial shipping fleet of its own, its massive naval expenditure disproportionately benefits foreign, allied shipping conglomerates and export-heavy nations that rely on secure oceans to reach global consumer markets.23

Therefore, the user’s hypothetical proposition—that the Western World should pay $1 trillion annually to the U.S. to offset the $38 trillion debt—is not an arbitrary figure. It represents a theoretical “geopolitical insurance premium,” a retroactive monetization of the defense subsidies, maritime security, and nuclear deterrence the United States has provided since the implementation of the Marshall Plan and the founding of NATO.16 By pooling this capital and transferring it directly to the U.S. Treasury, the allies would essentially be paying their deferred geopolitical dues, allowing the U.S. to rapidly deleverage its balance sheet without extracting further capital from its own domestic tax base.

The Macroeconomic Reality of the 2025-2026 Tariff Disruption

Rather than pursuing a cooperative, grant-based mechanism for debt reduction, the U.S. administration enacted a highly disruptive, unilateral tariff regime beginning in 2025. Driven by the “America First” trade doctrine and the desire to simultaneously punish geopolitical rivals, coerce allies, and generate federal revenue, the administration utilized a myriad of executive actions to erect massive protectionist walls.8 The administration initially invoked the International Emergency Economic Powers Act to impose sweeping global tariffs, driving the average effective tariff rate on U.S. imports from approximately 2.4 percent to a staggering 13.8 percent.8

When the U.S. Supreme Court struck down the use of IEEPA for tariff enforcement in February 2026, the administration immediately pivoted, utilizing Section 122 of the Trade Act of 1974 to impose a baseline 10 percent universal tariff on all countries, with specific reciprocal tariffs scaling up to 50 percent on targeted nations, and punitive duties exceeding 60 percent to 104 percent on China.8 The administration championed these tariffs as a mechanism to rebuild the U.S. manufacturing base, correct persistent trade deficits, and raise “trillions of dollars” to service the national debt and offset the sweeping tax cuts enacted in domestic legislation.45 However, rigorous macroeconomic analysis reveals that the tariff disruption has been highly deleterious, functioning as a regressive tax that harms the American consumer, slows economic growth, and alienates critical geopolitical allies.

The Illusion of Revenue and Severe Macroeconomic Drag

The primary political justification for the universal tariff regime was its potential to generate vast sums of federal revenue. Conventional, static scoring models suggested that a sweeping tariff plan could raise over $5.2 trillion over a decade.48 Indeed, in 2025, U.S. customs duties surged, generating an estimated $194.8 billion to $264 billion in new, inflation-adjusted revenue above historical averages.8

However, when analyzed through dynamic macroeconomic models—which account for behavioral shifts, the suppression of economic activity, and retaliatory measures by foreign governments—the revenue-generating capacity of tariffs is severely diminished. Tariffs function as a massive negative supply shock to the domestic economy. By artificially inflating the cost of imported intermediate goods, machinery, and raw materials, tariffs increase the marginal cost of domestic investment and severely reduce the efficiency of resource allocation.17

Consequently, the Penn Wharton Budget Model projects that the administration’s tariff policies will reduce long-run U.S. Gross Domestic Product by up to 0.6 percent, depress the capital stock by 1.3 percent, and lower average wages by as much as 5 percent over the long term.48 Similarly, the Tax Foundation estimates that the permanent application of Section 232 and Section 122 tariffs will actively shrink the U.S. economy, resulting in a loss of hundreds of thousands of full-time equivalent jobs.8 Because the tariffs suppress overall economic output, they inherently shrink the base for individual income and corporate payroll taxes. When accounting for these negative dynamic feedback loops, the actual net revenue generated for debt reduction falls drastically, with some estimates suggesting the 10-year net revenue yield drops to just $517 billion, a fraction of the conventionally scored estimates.8 Attempting to resolve a $38 trillion sovereign debt crisis through universal tariffs is mathematically inefficient; the policy destroys a significant portion of the underlying economic wealth it is attempting to tax, representing a highly distortive fiscal mechanism.48

The Devastating Incidence on the U.S. Household

The most profound failure of the 2025–2026 tariff strategy—and the reason it is accurately described as a “horrifying disruption”—lies in its economic incidence. Despite political rhetoric claiming that foreign nations pay the tariffs, empirical economic data categorically demonstrates that the cost of these import taxes is overwhelmingly absorbed by U.S. firms and passed directly through to American consumers.

Research analyzing millions of shipment records following the tariff hikes indicates that 90 to 96 percent of the tariff burden is borne by domestic buyers.44 Foreign exporters have largely refused to lower their unit prices to offset the duties; instead, U.S. importers pay the tax at the border and pass the increased costs onto the retail market.44 Consequently, tariffs function entirely as a regressive domestic consumption tax, disproportionately harming lower- and middle-income families who spend a larger share of their income on tradable goods.

The financial impact on the American populace has been severe and immediate. Due to the tariffs, the cost of imported personal consumption expenditures (PCE) for core goods and durable goods rose sharply, tracking significantly above historical pre-2025 trends.49 Various macroeconomic analyses, including those from the Yale Budget Lab and the Tax Foundation, calculate that these tariffs impose an immediate, direct annual cost of between $600 and $2,800 on the average U.S. household.8 When compounding the effects of higher prices, depressed capital formation, and lower wages over a lifetime, the Penn Wharton Budget Model estimates that a middle-income American household faces a staggering $22,000 lifetime loss due to the tariff regime—a loss twice as large as a revenue-equivalent increase in the corporate tax rate.48

Furthermore, tariffs have actively undermined the Federal Reserve’s efforts to stabilize the U.S. dollar’s purchasing power. Empirical studies attribute between 0.4 and 1.0 percentage points of annualized consumer price inflation directly to the tariff regime.55 Industries heavily exposed to imported materials, such as construction, electronics, agriculture, and apparel, have seen massive price spikes, severely impacting the affordability of basic necessities.53 By deliberately inflating the cost of goods during a period of pre-existing economic anxiety, the tariff policy actively worsens the cost-of-living crisis for the American public, entirely contradicting its stated goal of domestic economic revitalization.

Diplomatic Retaliation and the Fracturing of Global Alliances

The geopolitical consequences of the tariff disruption have been equally disastrous. By imposing sweeping, non-differentiated tariffs on long-standing allies under the guise of “national security” or “reciprocity,” the United States fundamentally fractured the diplomatic alliances that form the bedrock of the Western world. Viewing the tariffs as extortionate and legally unjustified, the European Union, Canada, and Mexico immediately enacted retaliatory countermeasures.

Canada applied 25 percent tariffs on billions of dollars of U.S. goods, the European Union prepared countermeasures targeting up to €93 billion worth of American exports, and China escalated its own duties on U.S. agriculture and energy products.60 This retaliatory spiral devastated U.S. export markets. American farmers and manufacturers bore the brunt of the trade war, as foreign buyers seamlessly substituted American products with alternatives from South America or Asia.14

The diplomatic fallout severely complicated broader U.S. strategic objectives. By treating mutual defense and economic cooperation as transactional and combative, the U.S. alienated key strategic partners precisely when unity was required to counter the rising influence of China and manage regional conflicts in Eastern Europe and the Middle East.65 G7 summits devolved into hostile, testy confrontations regarding the “Trump Turbulence Tax,” and nations like Canada and the EU began actively laying the groundwork to pivot their economic, technological, and security reliance away from the United States to ensure their own sovereignty.67 In sum, the tariff approach damaged the U.S. economy, impoverished American consumers, and isolated the nation geopolitically, all while generating suboptimal, economically destructive revenue for debt reduction.

| Economic Dimension | Impact of 2025-2026 U.S. Tariff Regime | Data Source & Mechanism |

| Household Cost | $600 to $2,800 direct annual tax per U.S. household; $22,000 lifetime loss for middle-income earners. | Passed through via higher retail prices on core goods and durables.8 |

| Inflation (CPI/PCE) | Adds 0.4 to 1.0 percentage points to annual inflation. | Import costs inflate domestic supply chains, negating Fed stabilization efforts.55 |

| GDP & Wages | Depresses long-run GDP by 0.2% to 0.6%; suppresses capital stock and labor hours. | Tariffs act as a negative supply shock, increasing the cost of investment.8 |

| Export Markets | Severe contraction due to foreign retaliatory tariffs. | EU, Canada, Mexico, and China substitute U.S. goods with foreign alternatives.14 |

| Debt Reduction | Highly inefficient; dynamic revenue falls to ~$517B over ten years. | The economic drag shrinks the income and payroll tax base, offsetting customs duty gains.8 |

Table 2: The Macroeconomic and Household Impact of the 2025-2026 U.S. Tariff Disruption.

The Hypothetical $1 Trillion Annual Grant: A Domestic Macroeconomic Panacea

Given the immense collateral damage, deadweight loss, and geopolitical alienation caused by the tariff regime, the user’s hypothetical proposition—a direct, non-repayable grant of $1 trillion annually for ten years, paid by the “Western World” to the United States—demands rigorous comparative analysis. This concept effectively operates as a “Reverse Marshall Plan”.16 Following World War II, the U.S. transferred massive capital to Europe to rebuild its infrastructure, stabilize its currencies, and secure democratic institutions against communism.16 Today, the proposal suggests a complete inversion of that historical flow: allied nations would transfer massive capital directly to the U.S. Treasury to underwrite the accumulated costs of the American military-industrial complex and stabilize the hegemonic debt that guarantees their continued prosperity.16

Setting aside the profound political and institutional barriers that render this proposal currently impossible to implement, evaluating it strictly as a hypothetical macroeconomic mechanism reveals that it is mathematically and functionally superior to tariffs for the purpose of domestic debt reduction. If the goal is to resolve the $38.86 trillion U.S. debt without destroying the domestic economy, the grant acts as a macroeconomic panacea.

1. Absolute Fiscal Efficiency and the Eradication of Deadweight Loss

The primary advantage of the hypothetical grant is its absolute fiscal efficiency. As established, tariffs attempt to reduce the sovereign debt by taxing domestic consumption and international trade, which creates severe deadweight loss. Tariffs destroy economic value by distorting market prices, disrupting efficient global supply chains, and causing the misallocation of capital.50 The Tax Foundation and Yale Budget Lab data explicitly demonstrate that tariffs extract capital directly from the disposable income of American citizens, forcing households to fund the debt reduction through higher prices at the checkout counter.8

Conversely, an external grant is an influx of foreign capital. It requires zero extraction from the American consumer. By relying on allied governments to transfer $1 trillion annually, the United States bypasses the $1,700 to $2,800 annual penalty imposed on domestic households by tariffs.53 The grant provides absolute, guaranteed deficit reduction without cannibalizing the U.S. income or payroll tax base. This $10 trillion injection over a decade would drastically alter the Congressional Budget Office’s baseline projections, rapidly deleveraging the government’s balance sheet without requiring domestic tax hikes or draconian cuts to critical entitlement programs like Social Security or Medicare.74

2. Disinflationary Mechanics and the Reduction of Net Interest

While tariffs are inherently inflationary, adding up to 1.0 percentage point to the CPI 55, the hypothetical $1 trillion annual grant would be highly disinflationary. If the U.S. Treasury receives $1 trillion in pure cash annually and uses it exclusively to retire outstanding sovereign debt, the supply of marketable U.S. bonds would shrink rapidly.

A sharp reduction in the supply of government debt, assuming demand remains somewhat constant, inherently drives bond prices up and pushes bond yields (interest rates) down.76 This dynamic would trigger a massive, compounding fiscal dividend. Currently, the U.S. is projected to spend over $16.2 trillion on net interest payments over the next decade.6 By utilizing the grant to wipe out $10 trillion in principal, the U.S. Treasury would save hundreds of billions of dollars annually in compounding interest costs.

Furthermore, lower yields on Treasury bonds dictate the interest rates across the entire U.S. economy. Lower federal borrowing costs would translate directly into lower mortgage rates for American homebuyers, lower auto loan rates, and reduced borrowing costs for U.S. corporations.76 This environment of cheap, accessible capital would spur organic domestic investment, business expansion, and job creation, completely avoiding the capital stock decay and economic uncertainty generated by the “Trump Turbulence Tax”.48

3. The Preservation of U.S. Export Markets and Geopolitical Harmony

Because the hypothetical grant replaces the need for aggressive trade protectionism, it eliminates the catalyst for foreign retaliation. If the U.S. abandons its universal tariffs in exchange for this allied security payment, U.S. agricultural, technological, and manufacturing sectors would retain unfettered, tariff-free access to global consumer markets. The devastating export destruction witnessed during the 2025–2026 trade conflicts—where China, the EU, and Canada systematically targeted American farmers and industrial producers—would be entirely avoided.14

Diplomatically, while convincing allies to pay $1 trillion a year would be an unprecedented diplomatic hurdle, if achieved consensually, it would represent a unified, cooperative recognition of America’s security umbrella. It would replace the hostility of unpredictable trade wars with a structured, predictable system of international burden-sharing, theoretically preserving the cohesiveness of NATO and the broader Western alliance.34

| Evaluation Metric | The 2025-2026 Universal Tariff Reality | The Hypothetical $1T Annual Allied Grant | Comparative Domestic Advantage |

| 10-Year Debt Reduction | ~$517B to $4.5T (Cannibalized by economic drag) | $10.0T (Absolute, guaranteed external capital) | Grant provides more than double the fiscal relief without tax base erosion. |

| U.S. Household Impact | Regressive cost of $1,700 – $2,800 / year | $0 direct domestic cost | Grant completely shields domestic consumers from debt-reduction costs. |

| Inflationary Effect | Highly inflationary; adds 0.5% – 1.0% to CPI | Disinflationary; lowers Treasury yields | Grant stabilizes consumer prices and lowers nationwide borrowing costs. |

| GDP Impact (Long-term) | Contracts GDP by 0.2% – 0.6% | Expands GDP via lower interest rates | Grant avoids deadweight loss and promotes capital formation. |

| Export Market Access | Severely damaged by immediate foreign retaliation | Fully preserved | Grant avoids retaliatory tariffs on U.S. agricultural and industrial goods. |

Table 3: Comparative Macroeconomic Evaluation of Sovereign Debt Reduction Strategies on the U.S. Domestic Economy. 8

From a strictly domestic, first-order macroeconomic perspective, the user’s hypothesis is entirely correct: the $1 trillion annual grant acts as a vastly superior, friendlier, and cheaper mechanism for the American public. It solves the sovereign debt crisis mathematically, preserves the purchasing power of the U.S. dollar, lowers interest rates, and shields the American consumer from the agonizing costs and inefficiencies of trade protectionism.

Global Systemic Repercussions: Why the “Better” Option is Globally Catastrophic

If the hypothetical grant is mathematically and domestically superior to tariffs, why did the analytical framework in the provided source material explicitly state that it was “impossible in the current world order”?15 The answer lies beyond the political difficulty of convincing foreign nations to pay tribute. The impossibility is rooted in the profound, third-order macroeconomic shocks that extracting $1 trillion annually from allied economies and suddenly retiring $10 trillion in U.S. debt would inflict upon the global financial architecture.

While tariffs represent a blunt, damaging instrument that the world can painfully adapt to (by rerouting supply chains and substituting goods), the hypothetical grant acts as a systemic wrecking ball to global dollar liquidity and allied economic stability. The United States does not operate in an economic vacuum, and fixing its balance sheet at the expense of the rest of the world carries catastrophic global consequences.

1. The “Safe Asset” Paradox and the Collapse of Global Dollar Liquidity

The most critical insight regarding the U.S. national debt is that it is not merely a domestic liability; it is the foundational collateral of the entire global financial system. According to macroeconomic theorists like Ricardo Caballero, the global economy suffers from a structural “safe asset shortage”.80 Emerging markets, multinational corporations, sovereign wealth funds, and foreign central banks generate vast amounts of capital through trade surpluses, but they lack the institutional mechanisms to store that wealth safely within their own borders. Therefore, they export their savings to the United States, purchasing U.S. Treasury securities, which serve as the world’s ultimate, indispensable risk-free asset.80

Over $8.5 trillion of the U.S. public debt is currently held in foreign accounts.84 Treasuries are utilized globally to manage interest rate risk, value other securities, and, most importantly, function as the primary collateral in overnight repurchase (repo) markets, which dictate global dollar liquidity.85

If the United States were to suddenly receive $10 trillion in allied grants over a decade and use it to rapidly retire sovereign debt, the supply of available U.S. Treasuries would undergo an unprecedented, violent contraction. This would drastically exacerbate the global safe asset shortage. As the supply of Treasuries collapses against sustained global demand, their prices would skyrocket, driving yields to zero or into negative territory. This phenomenon—known as a severe compression of the “convenience yield”—would signal a desperate global scramble for collateral.87

The historical precedent for a safe asset shortage is alarming. In the late 1990s and early 2000s, when the U.S. briefly ran budget surpluses and reduced debt issuance, global demand for safe assets vastly outstripped supply. To fill the void, the global shadow banking system began utilizing dangerous financial engineering. Financial institutions pooled inherently risky assets (such as subprime mortgages, auto loans, and credit card receivables) and tranched them to create synthetic, AAA-rated “safe” assets to satisfy global demand.80 When investors eventually realized these synthetic assets were inherently flawed and far from risk-free, the entire system collapsed, resulting in the 2008 Global Financial Crisis.80

By aggressively retiring $10 trillion in debt through external grants, the hypothetical proposal would drain global financial markets of their primary, stabilizing safe asset. This artificial contraction would almost certainly incentivize a rapid return to dangerous financial engineering, risking a catastrophic global liquidity freeze and severe financial instability.15 In essence, the U.S. national debt is the grease that keeps the wheels of global finance turning; removing it too quickly seizes the engine.

2. Allied Austerity, Export Destruction, and the Paradox of Thrift

Beyond the highly technical plumbing of the Treasury market, the physical extraction of $1 trillion annually from the economies of Western Europe, Japan, Canada, and Australia would trigger devastating macroeconomic consequences in the real economy.

To fund a $1 trillion annual non-repayable grant to the United States, allied governments would be forced to implement draconian fiscal austerity measures. They would have to drastically raise their own domestic taxes, gut their social welfare states, and slash their infrastructure and independent defense spending to generate the capital required to pay the U.S. Treasury. This massive, sustained drain of capital would plunge the European Union and East Asian economies into deep, protracted economic depressions.90

Herein lies the fatal flaw of the hypothetical model: the United States cannot thrive if its partners are destitute. The U.S. economy relies heavily on robust foreign demand from these very allies to purchase its agricultural exports, technological services, and manufactured goods. If the economies of its closest allies are hollowed out to pay the $1 trillion annual tribute, global demand will completely collapse.

The resulting global recession would invariably boomerang back onto the United States. Without wealthy foreign consumers to buy American products, U.S. export industries would face obliteration, prompting massive domestic layoffs, corporate bankruptcies, and a severe contraction of the U.S. tax base. Thus, the macroeconomic “Paradox of Thrift” applies: by forcing allies to aggressively transfer their wealth to pay down U.S. debt, the resulting global economic contraction would plunge the U.S. into a recession, ultimately reducing federal revenues and potentially expanding the deficit the grant was meant to eliminate.15

3. The Collapse of the Geopolitical Security Architecture

Finally, the geopolitical ramifications of coercing allies into paying a $1 trillion annual grant would fundamentally alter the nature of Western alliances, destroying the very Pax Americana the policy attempts to monetize. Historically, the U.S. has maintained its global hegemony by providing public goods—such as naval security, stable reserve currency, and nuclear deterrence—that make the international system profitable and secure for its allies. This mutual profitability ensures voluntary compliance with U.S. leadership and values.

If the United States transitions from a benevolent underwriter of global security to an aggressive extractor of financial tribute, the alliances shift from mutual defense pacts to protection rackets.90 The domestic populations of European and Asian democracies would almost certainly rebel against political leaders who authorize sending hundreds of billions of taxpayer dollars to Washington annually while their own domestic programs face severe austerity.

The political backlash would lead to the rapid disintegration of NATO and Pacific security treaties.65 Allies would be forced to aggressively decouple from the U.S. financial, technological, and security systems to preserve their own sovereignty. This would likely result in the balkanization of the global order, the rise of competing regional hegemons (such as a highly militarized Europe or an ascendant China), and the accelerated decline of the U.S. dollar as the world’s primary reserve currency.69 Ultimately, extracting $10 trillion in grants would cost the United States its position as the leader of the free world.

Conclusion: Evaluating the Optimal Pathway to Fiscal Stability

The foundational inquiry of this report rests on a theoretical premise: setting aside the real-world institutional and political impossibility of its implementation, would a $1 trillion annual grant from allied nations have been a much better, friendlier, and cheaper way of dealing with the $38.86 trillion U.S. debt compared to the horrifying disruption of the 2025–2026 universal tariffs?

When analyzed strictly through the lens of domestic, first-order macroeconomic impacts on the American household, the answer is unequivocally yes. The implementation of universal tariffs has proven to be a highly inefficient and destructive mechanism for sovereign debt reduction. Tariffs have functioned as a massive, regressive tax on the American consumer, driving up inflation, suppressing long-term GDP growth, eroding the purchasing power of the middle class, and inviting devastating retaliatory measures against U.S. exporters. Furthermore, the dynamic economic drag created by tariffs severely cannibalizes their own revenue-generating potential, rendering them mathematically incapable of solving a $38 trillion debt crisis.

Conversely, a $1 trillion annual external grant would theoretically bypass every negative consequence of the tariff regime. It would provide absolute, guaranteed deficit reduction without extracting a single dollar from American households. It would preserve the purchasing power of the U.S. consumer, alleviate inflationary pressures by lowering the supply of outstanding bonds (thereby decreasing nationwide interest rates), and maintain open access to global export markets by avoiding a retaliatory trade war. It would successfully and efficiently monetize the immense, uncompensated costs the United States has borne for eighty years in maintaining the global security architecture. For the American citizen, the grant represents a macroeconomic panacea.

However, macroeconomic policy cannot be isolated from the complex web of global financial interdependence. When the inevitable second and third-order systemic effects are integrated into the analysis, the hypothetical grant reveals itself to be a global hazard of unparalleled magnitude. The international financial architecture relies absolutely on the continued issuance and availability of U.S. Treasury securities to function as the bedrock of global liquidity and safe collateral. Violently extracting $10 trillion in debt from the market would trigger an acute safe asset shortage, paralyzing global capital flows and potentially inciting a shadow-banking collapse reminiscent of 2008. Furthermore, draining $1 trillion annually from allied economies would plunge the developed world into a severe, protracted recession, destroying global demand for U.S. exports and ultimately dragging the American economy into the very economic abyss the grant was designed to avoid.

Ultimately, while the tariff regime has burdened the American populace with inflation and economic drag, it represents a profound friction that the global economy can—and historically has—adapted to, albeit painfully, through the rerouting of supply chains and price adjustments. The hypothetical allied grant, while undeniably a far “cheaper and friendlier” solution for the average American household on paper, would fundamentally break the mechanics of global dollar liquidity and allied economic stability, destroying the Western alliance in the process. Therefore, the resolution to the $38.86 trillion U.S. sovereign debt crisis cannot be sustainably achieved through either punitive global taxation (tariffs) or coercive global tribute (grants); it must invariably rely on the agonizing but necessary process of internal fiscal consolidation, domestic entitlement reform, and a calibrated, cooperative reassessment of international defense expenditures.

Works cited

- The Consequences of Debt | The U.S. House Committee on the Budget, accessed March 29, 2026, https://budget.house.gov/press-release/the-consequences-of-debt

- Debt Dashboard – U.S. Congress Joint Economic Committee, accessed March 29, 2026, https://www.jec.senate.gov/public/index.cfm/republicans/debt-dashboard

- Monthly-Debt-Update-website.knit, accessed March 29, 2026, https://www.jec.senate.gov/public/vendor/_accounts/JEC-R/debt/Monthly%20Debt%20Update.html

- Interest on the Debt Surging Past National Defense – EPIC for America, accessed March 29, 2026, https://epicforamerica.org/federal-budget/interest-on-the-debt-surging-past-national-defense/

- US National Debt Hits $39 Trillion: What It Means for You and the Economy, accessed March 29, 2026, https://www.us-debt-clock.com/blog/us-debt-hits-39-trillion

- Interest Costs on the National Debt – Peterson Foundation, accessed March 29, 2026, https://www.pgpf.org/programs-and-projects/fiscal-policy/monthly-interest-tracker-national-debt/

- The U.S. Got Out from Crippling Levels of Federal Debt Before, and It Can Do It Again, accessed March 29, 2026, https://www.rand.org/pubs/commentary/2025/11/the-us-got-out-from-crippling-levels-of-federal-debt.html

- Tracking the Impact of the Trump Tariffs & Trade War – Tax Foundation, accessed March 29, 2026, https://taxfoundation.org/research/all/federal/trump-tariffs-trade-war/

- US Tariffs: What’s the Impact? | J.P. Morgan Global Research, accessed March 29, 2026, https://www.jpmorgan.com/insights/global-research/current-events/us-tariffs

- Fact Sheet: President Donald J. Trump Declares National Emergency to Increase our Competitive Edge, Protect our Sovereignty, and Strengthen our National and Economic Security – The White House, accessed March 29, 2026, https://www.whitehouse.gov/fact-sheets/2025/04/fact-sheet-president-donald-j-trump-declares-national-emergency-to-increase-our-competitive-edge-protect-our-sovereignty-and-strengthen-our-national-and-economic-security/

- The Changing Tariffs Landscape: What We Know, What We Think We Know, What We Don’t Know, accessed March 29, 2026, https://www.globaltrademag.com/the-changing-tariffs-landscape-what-we-know-what-we-think-we-know-what-we-dont-know/

- Trump announces a universal 10% tariff: what effects will it have on the economy? – Mapfre, accessed March 29, 2026, https://www.mapfre.com/en/insights/economy/trump-tariffs-effects-economy/

- In Tariffs Debate, Gen Z and Millennials Favor Lower Prices and More Choices, accessed March 29, 2026, https://globalaffairs.org/research/public-opinion-survey/tariffs-debate-gen-z-and-millennials-favor-lower-prices-and-more

- Separating Tariff Facts from Tariff Fictions – Cato Institute, accessed March 29, 2026, https://www.cato.org/publications/separating-tariff-facts-tariff-fictions

- Macro-Financial Imbalances and Institutional Attrition_ A Comparative Analysis of U.S. Debt Hegemony and Systemic Rigidity in the Islamic World – Hans Smedema Affair.pdf

- The Marshall Plan in Reverse – The Philosophical Salon, accessed March 29, 2026, https://thephilosophicalsalon.com/the-marshall-plan-in-reverse/

- The Budget and Economic Outlook: 2026 to 2036 | Congressional Budget Office, accessed March 29, 2026, https://www.cbo.gov/publication/62105

- The $88 Trillion Unfunded Entitlement Obligation Washington Keeps Ignoring, accessed March 29, 2026, https://www.cato.org/blog/88-trillion-unfunded-entitlement-obligation-washington-keeps-ignoring-0

- Report: America’s $38 Trillion Debt Demands Bipartisan Action – The Conference Board, accessed March 29, 2026, https://www.conference-board.org/press/americas-38-trillion-dollar-debt-demands-bipartisan-action

- US Fiscal Dominance, the Coming Fiscal Inflection Point, and How Congress Can Fix the Debt Crisis (Before It’s Too Late) – Cato Institute, accessed March 29, 2026, https://www.cato.org/blog/us-fiscal-dominance-coming-fiscal-inflection-point-how-congress-can-fix-debt-crisis-its-too

- Sea Power: The U.S. Navy and Foreign Policy, accessed March 29, 2026, https://www.cfr.org/backgrounders/sea-power-us-navy-and-foreign-policy

- Bad Idea: Assuming Trade Depends on the Navy – Defense360 – CSIS, accessed March 29, 2026, https://defense360.csis.org/bad-idea-assuming-trade-depends-on-the-navy/

- It’s Time for a Comprehensive National Maritime Strategy – War on the Rocks, accessed March 29, 2026, https://warontherocks.com/2024/03/its-time-for-a-comprehensive-national-maritime-strategy/

- The United States Sea Services Contributions To Our National, Individual, And Business Prosperity – KC Chamber, accessed March 29, 2026, https://www.kcchamber.com/current-topics/the-united-states-sea-services-contributions-to-our-national-individual-and-business-prosperity/

- G7 Foreign Ministers Declaration on Maritime Security and Prosperity, accessed March 29, 2026, https://asean.usmission.gov/g7-foreign-ministers-declaration-on-maritime-security-and-prosperity/

- U.S. Federal Budget | Costs of War – Brown University, accessed March 29, 2026, https://costsofwar.watson.brown.edu/costs/economic/us-federal-budget

- Costs of War | Brown University, accessed March 29, 2026, https://costsofwar.watson.brown.edu/

- NATO’s Underspending Problem: America’s Allies Must Embrace Fair Burden Sharing, accessed March 29, 2026, https://www.heritage.org/defense/report/natos-underspending-problem-americas-allies-must-embrace-fair-burden-sharing

- Rethinking the NATO burden-sharing debate – Atlantic Council, accessed March 29, 2026, https://www.atlanticcouncil.org/blogs/new-atlanticist/rethinking-the-nato-burden-sharing-debate/

- Why the National Debt Matters for National Security – Bipartisan Policy Center, accessed March 29, 2026, https://bipartisanpolicy.org/explainer/why-the-national-debt-matters-for-national-security/

- U.S. Defense Spending in Historical and International Context | Econofact, accessed March 29, 2026, https://econofact.org/u-s-defense-spending-in-historical-and-international-context

- NATO is Vital to U.S. National Security – Belfer Center, accessed March 29, 2026, https://www.belfercenter.org/research-analysis/nato-vital-us-national-security

- Revisiting the Value of the U.S. Nuclear Umbrella in East Asia – War on the Rocks, accessed March 29, 2026, https://warontherocks.com/2018/03/revisiting-value-u-s-nuclear-umbrella-east-asia/

- From Burden Sharing to Responsibility Sharing – CSIS, accessed March 29, 2026, https://www.csis.org/analysis/burden-sharing-responsibility-sharing

- Burdensharing and Its Discontents: Understanding and Optimizing Allied Contributions to the Collective Defense – RAND, accessed March 29, 2026, https://www.rand.org/content/dam/rand/pubs/research_reports/RR4100/RR4189z1/RAND_RR4189z1.pdf

- What Do U.S. Allies Really Contribute to the Costs of Global Security? – RAND, accessed March 29, 2026, https://www.rand.org/pubs/commentary/2025/01/what-do-us-allies-really-contribute-to-the-costs-of.html

- The Economic & Fiscal Impacts of U.S. Defense Spending in 2026 and Beyond, accessed March 29, 2026, https://economics.td.com/us-defense-spending-impacts

- The National Strategy for Maritime Security – the White House, accessed March 29, 2026, https://georgewbush-whitehouse.archives.gov/homeland/maritime.html

- The State of Maritime Supply-Chain Threats – CSIS, accessed March 29, 2026, https://www.csis.org/analysis/state-maritime-supply-chain-threats

- Applying the Law of the Sea to Protect International Shipping – the United Nations, accessed March 29, 2026, https://www.un.org/en/un-chronicle/applying-law-sea-protect-international-shipping

- Postwar Planning Must Begin: What a Modern Marshall Plan for Ukraine Looks Like, accessed March 29, 2026, https://www.gmfus.org/news/postwar-planning-must-begin-what-modern-marshall-plan-ukraine-looks

- Cybersecurity Insurance: Modeling and Pricing – SOA, accessed March 29, 2026, https://www.soa.org/globalassets/assets/files/research/projects/cybersecurity-insurance-report.pdf

- Regulating Imports with a Reciprocal Tariff to Rectify Trade Practices that Contribute to Large and Persistent Annual United States Goods Trade Deficits, accessed March 29, 2026, https://www.whitehouse.gov/presidential-actions/2025/04/regulating-imports-with-a-reciprocal-tariff-to-rectify-trade-practices-that-contribute-to-large-and-persistent-annual-united-states-goods-trade-deficits/

- Who Is Paying for the 2025 U.S. Tariffs? – Liberty Street Economics, accessed March 29, 2026, https://libertystreeteconomics.newyorkfed.org/2026/02/who-is-paying-for-the-2025-u-s-tariffs/

- “Liberation Day” Tariffs Explained – CSIS, accessed March 29, 2026, https://www.csis.org/analysis/liberation-day-tariffs-explained

- ‘Liberation Day,’ One Year Later, accessed March 29, 2026, https://thedispatch.com/article/liberation-day-tariffs-trump-economy/?utm_source=google-news&utm_medium=syndication

- Tariffs “Funded” Everything in 2025—Will the Fantasy Continue in 2026? [UPDATE: Apparently, It Will] | Cato at Liberty Blog, accessed March 29, 2026, https://www.cato.org/blog/tariffs-funded-everything-2025-will-fantasy-continue-2026

- The Economic Effects of President Trump’s Tariffs | Penn Wharton Budget Model, accessed March 29, 2026, https://budgetmodel.wharton.upenn.edu/p/2025-04-10-the-economic-effects-of-president-trumps-tariffs/

- Tracking the Economic Effects of Tariffs | The Budget Lab at Yale, accessed March 29, 2026, https://budgetlab.yale.edu/research/tracking-economic-effects-tariffs

- The Fed – Trade-offs of Higher U.S. Tariffs: GDP, Revenues, and the Trade Deficit, accessed March 29, 2026, https://www.federalreserve.gov/econres/notes/feds-notes/trade-offs-of-higher-u-s-tariffs-gdp-revenues-and-the-trade-deficit-20250707.html

- Working Paper 25-19: Tariffs as fiscal policy – Peterson Institute for International Economics, accessed March 29, 2026, https://www.piie.com/sites/default/files/2025-09/wp25-19.pdf

- America’s own goal: Americans pay almost entirely for Trump’s tariffs – Kiel Institute, accessed March 29, 2026, https://www.kielinstitut.de/publications/news/americas-own-goal-americans-pay-almost-entirely-for-trumps-tariffs/

- State of U.S. Tariffs: July 14, 2025 | The Budget Lab at Yale, accessed March 29, 2026, https://budgetlab.yale.edu/research/state-us-tariffs-july-14-2025

- Here’s how much tariffs are costing US families each month, according to Democrats, accessed March 29, 2026, https://www.fox29.com/news/how-much-tariffs-cost-us-families-monthly

- A Year in Review: How the Trump Administration’s Economic Policies Made Life Less Affordable for Americans, accessed March 29, 2026, https://www.americanprogress.org/article/a-year-in-review-how-the-trump-administrations-economic-policies-made-life-less-affordable-for-americans/

- Tariff troubles: Could protectionism revive stagflation? | EY – Global, accessed March 29, 2026, https://www.ey.com/en_pl/insights/strategy/macroeconomics/macro-tariff-playbook-reciprocal-tariffs

- How Tariffs Are Affecting Prices in 2025 | St. Louis Fed, accessed March 29, 2026, https://www.stlouisfed.org/on-the-economy/2025/oct/how-tariffs-are-affecting-prices-2025

- Tariff policies in 2025 increased input costs for key U.S. industries, threatening growth and investment, accessed March 29, 2026, https://equitablegrowth.org/tariff-policies-in-2025-increased-input-costs-for-key-u-s-industries-threatening-growth-and-investment/

- Seven in 10 Americans say Trump tariffs have cost them more money – The Guardian, accessed March 29, 2026, https://www.theguardian.com/us-news/2026/mar/13/trump-tariffs-poll

- 2025–2026 United States trade war with Canada and Mexico – Wikipedia, accessed March 29, 2026, https://en.wikipedia.org/wiki/2025%E2%80%932026_United_States_trade_war_with_Canada_and_Mexico

- US tariffs: economic, financial and monetary repercussions – European Parliament, accessed March 29, 2026, https://www.europarl.europa.eu/RegData/etudes/IDAN/2025/764382/ECTI_IDA(2025)764382_EN.pdf

- Trump 2.0 tariff tracker, accessed March 29, 2026, https://www.tradecomplianceresourcehub.com/2026/03/24/trump-2-0-tariff-tracker/

- The implications of US-China trade tensions for the euro area – lessons from the tariffs imposed by the first Trump Administration – European Central Bank, accessed March 29, 2026, https://www.ecb.europa.eu/press/economic-bulletin/focus/2025/html/ecb.ebbox202503_02~b2916b44db.en.html

- Navigating the storm: Southeast Asia and the global trade shocks | Lowy Institute, accessed March 29, 2026, https://www.lowyinstitute.org/publications/navigating-storm-southeast-asia-global-trade-shocks

- President Trump’s tariffs increase pressure on allies to reduce security dependence on the US | Chatham House, accessed March 29, 2026, https://www.chathamhouse.org/2025/04/president-trumps-tariffs-increase-pressure-allies-reduce-security-dependence-us

- From Geoeconomics to Trump’s Geopolitics – CEBRI, accessed March 29, 2026, https://cebri.org/revista/en/artigo/195/from-geoeconomics-to-trumps-geopolitics

- Geopolitics of Trump Tariffs: How U.S. Trade Policy Has Shaken Allies, accessed March 29, 2026, https://www.cfr.org/articles/geopolitics-trump-tariffs-how-us-trade-policy-has-shaken-allies

- Trump’s tariffs will test U.S. allies at G7 finance ministers’ summit | PBS News, accessed March 29, 2026, https://www.pbs.org/newshour/economy/trumps-tariffs-will-test-u-s-allies-at-g7-finance-ministers-summit

- Canada Lays the Groundwork to Pivot Away From the United States, accessed March 29, 2026, https://www.cfr.org/articles/canada-lays-groundwork-pivot-away-united-states

- 8 Ways Trump’s Turbulence Tax Is Costing the Economy – Center for American Progress, accessed March 29, 2026, https://www.americanprogress.org/article/8-ways-trumps-turbulence-tax-is-costing-the-economy/

- The Marshall Plan and Postwar Economic Recovery | The National WWII Museum | New Orleans, accessed March 29, 2026, https://www.nationalww2museum.org/war/articles/marshall-plan-and-postwar-economic-recovery

- Keystones for the Future: Unlocking Global Governance Failures of Yesterday and Today, accessed March 29, 2026, https://metapolis.net/project/keystones-for-the-future-unlocking-global-governance-failures-of-yesterday-and-today-3/

- State of U.S. Tariffs: November 17, 2025 | The Budget Lab at Yale, accessed March 29, 2026, https://budgetlab.yale.edu/research/state-us-tariffs-november-17-2025

- Policy Options for Reducing the Federal Debt: Spring, 2024 | Penn Wharton Budget Model, accessed March 29, 2026, https://budgetmodel.wharton.upenn.edu/p/2024-04-22-policy-options-for-reducing-the-federal-debt-spring-2024/

- Long-term Impacts of the One Big Beautiful Bill Act | The Budget Lab at Yale, accessed March 29, 2026, https://budgetlab.yale.edu/research/long-term-impacts-one-big-beautiful-bill-act

- Why the National Debt Matters for the U.S. Bond Market and the Economy, accessed March 29, 2026, https://bipartisanpolicy.org/explainer/why-the-national-debt-matters-for-the-u-s-bond-market-and-the-economy/

- Here’s How Countries Are Retaliating Against Trump’s Tariffs – WITA, accessed March 29, 2026, https://www.wita.org/atp-research/how-countries-retaliating-tariffs/

- Financial Stability Review, May 2025 – European Central Bank, accessed March 29, 2026, https://www.ecb.europa.eu/press/financial-stability-publications/fsr/html/ecb.fsr202505~0cde5244f6.en.html

- Where We Stand: The Fiscal, Economic, and Distributional Effects of All U.S. Tariffs Enacted in 2025 Through April 2 | The Budget Lab at Yale, accessed March 29, 2026, https://budgetlab.yale.edu/research/where-we-stand-fiscal-economic-and-distributional-effects-all-us-tariffs-enacted-2025-through-april

- A Global Safe Asset Shortage – Western Asset, accessed March 29, 2026, https://www.westernasset.com/US/en/pdfs/commentary/GlobalSafeAssetShortage201007.pdf

- 26 Global Safe Asset Shortage: The Role of Central Banks – MIT Economics, accessed March 29, 2026, https://economics.mit.edu/sites/default/files/inline-files/Global%20Safe%20Asset%20Shortage-%20The%20Role%20of%20Central%20Banks.pdf

- Fragility of Safe Asset Markets – Office of Financial Research (OFR), accessed March 29, 2026, https://www.financialresearch.gov/working-papers/files/OFRwp-23-02_fragility-of-safe-asset-markets.pdf

- Foreign Safe Asset Demand and the Dollar Exchange Rate – NBER, accessed March 29, 2026, https://www.nber.org/system/files/working_papers/w24439/revisions/w24439.rev1.pdf

- Foreign Investors Hold a Shrinking Share of U.S. Debt – Bipartisan Policy Center, accessed March 29, 2026, https://bipartisanpolicy.org/article/foreign-investors-hold-a-shrinking-share-of-u-s-debt/

- How Has Treasury Market Liquidity Fared in 2025? – Liberty Street Economics, accessed March 29, 2026, https://libertystreeteconomics.newyorkfed.org/2025/11/how-has-treasury-market-liquidity-fared-in-2025/

- US Treasury market conditions and global market reactions to US monetary policy – European Central Bank, accessed March 29, 2026, https://www.ecb.europa.eu/press/economic-bulletin/focus/2024/html/ecb.ebbox202308_01~352236489b.en.html

- Are US Treasuries still a safe haven? – State Street, accessed March 29, 2026, https://www.statestreet.com/web/insights/articles/documents/the-great-repricing-us-treasuries-still-safe-haven.pdf

- Decoupling Dollar and Treasury Privilege – International Monetary Fund, accessed March 29, 2026, https://www.imf.org/-/media/files/news/seminars/2025/26th-annual-research-conference/drafts/decoupling-dollar-and-treasury-privilege.pdf

- Safe Assets in Emerging Market Economies – American Economic Association, accessed March 29, 2026, https://www.aeaweb.org/conference/2025/program/paper/fiyE8Y58

- Trillion Dollar Bills: The Costs of Transatlantic Dependence for Europe, accessed March 29, 2026, https://transitionsecurity.org/trillion-dollar-bills/

- US tariffs will intensify debt crisis in lower-income countries – Debt Justice, accessed March 29, 2026, https://debtjustice.org.uk/blog/us-tariffs-will-intensify-debt-crisis-in-lower-income-countries

- What Would a Fiscal Crisis Look Like? | Committee for a Responsible Federal Budget, accessed March 29, 2026, https://www.crfb.org/papers/what-would-fiscal-crisis-look

- Trump and the Transatlantic Alliance: Greenland, Tariffs, and NATO Under Strain, accessed March 29, 2026, https://trendsresearch.org/insight/trump-and-the-transatlantic-alliance-greenland-tariffs-and-nato-under-strain/

- De-dollarization: The end of dollar dominance? – J.P. Morgan, accessed March 29, 2026, https://www.jpmorgan.com/insights/global-research/currencies/de-dollarization

- How to dismantle a reserve currency – Atlantic Council, accessed March 29, 2026, https://www.atlanticcouncil.org/in-depth-research-reports/issue-brief/how-to-dismantle-a-reserve-currency/