Last Updated 29/03/2026 published 29/03/2026 by Hans Smedema

Page Content

Structural Reconfiguration of Global Safe Assets and Sovereign Debt: A Macroeconomic Blueprint for the Transatlantic and Pacific Alliance

Google Gemini 3.1 Pro Deep Research Report based on the earlier Reports:

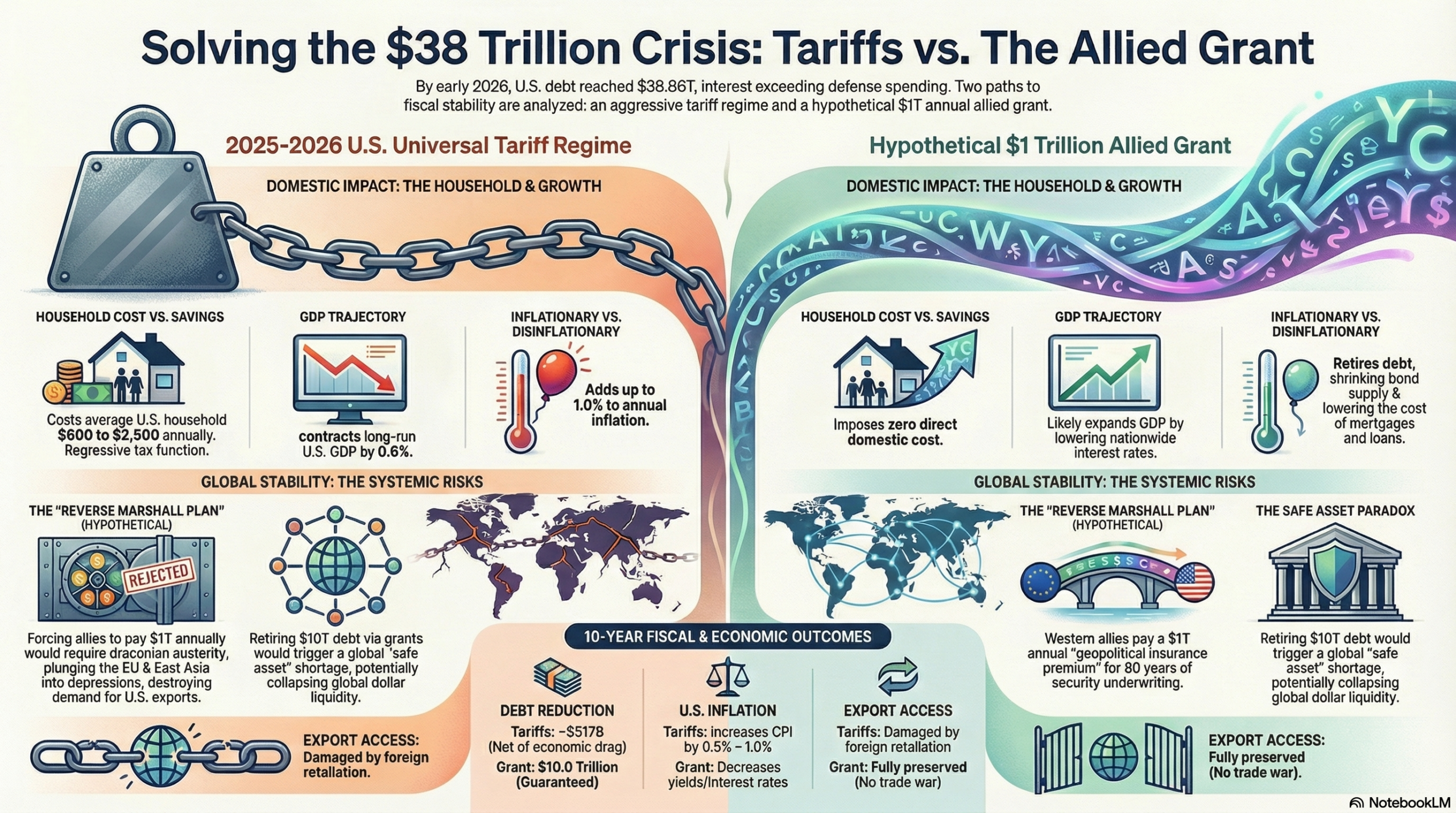

The trajectory of the United States sovereign debt, which decisively breached the $38.86 trillion threshold in early 2026, has precipitated an unprecedented crisis in both domestic macroeconomic policy and the broader architecture of global finance.1 With the debt-to-gross domestic product (GDP) ratio surpassing 122 percent and annualized net interest expenses exceeding the $1 trillion mark—thereby officially eclipsing the entirety of the U.S. national defense budget—traditional avenues of fiscal consolidation have been largely exhausted by structural rigidities and political paralysis.1 In an attempt to address this paralyzing fiscal burden, the U.S. administration deployed a highly aggressive, protectionist trade agenda throughout 2025 and 2026. This strategy, characterized by near-universal tariffs, was ostensibly designed to generate trillions in federal revenue and protect domestic manufacturing.1 However, the systemic frictions introduced by this tariff regime have severely compromised domestic economic vitality, resulting in profound deadweight loss, inflation, and global supply chain fragmentation.3

In evaluating theoretical alternatives to the current tariff disruption, a paradigm grounded in Hegemonic Stability Theory has been proposed: a $1 trillion annual security grant provided by a coalition of advanced allied nations to the United States to retroactively compensate for the historical costs of underwriting global security and maritime stability.1 Early orthodox critiques of this proposal argued that such a massive external capital transfer would trigger two catastrophic global outcomes: first, an “allied austerity” crisis that would plunge the developed world into a severe, protracted recession, and second, an acute “safe asset shortage” wherein the rapid retirement of U.S. Treasury securities would paralyze global capital flows and incite a shadow-banking collapse reminiscent of 2008.1

This report provides an exhaustive, contrarian macroeconomic re-evaluation of these critiques. By rigorously analyzing current global GDP capacity and moving beyond static models of global finance, this analysis deconstructs the failures of the universal tariff regime and empirically validates the capacity of allied economies to shoulder the costs of global security. Furthermore, it directly challenges the orthodox assumption that U.S. debt consolidation must inevitably trigger a safe asset shortage. By architecting a suite of novel financial mechanisms—ranging from the mutualized issuance of Allied Security Bonds and the capitalization of a U.S. Sovereign Wealth Fund to the modernization of the International Monetary Fund (IMF) Substitution Account—this report demonstrates how a $1 trillion annual geopolitical stabilization transfer can be executed efficiently without fracturing the bedrock of global dollar liquidity.

The Macroeconomic Devastation of the 2025-2026 Universal Tariff Regime

The primary fiscal strategy deployed to offset the burgeoning U.S. sovereign debt crisis and address trade imbalances was the erection of a sweeping, unilateral tariff architecture. Utilizing a myriad of executive authorities, the U.S. administration fundamentally altered the terms of global trade. The initial invocation of the International Emergency Economic Powers Act (IEEPA) imposed sweeping global tariffs, driving the average effective tariff rate on U.S. imports from approximately 2.4 percent to a staggering 13.8 percent—the highest level since 1947.1 When the U.S. Supreme Court struck down the use of IEEPA for tariff enforcement in February 2026 (in Learning Resources, Inc. v. Trump), the administration immediately pivoted to utilizing Section 122 of the Trade Act of 1974 to impose a baseline 10 percent universal tariff on all countries, maintaining the effective tariff rate at approximately 10.3 percent.2

The Illusion of Revenue and Dynamic Macroeconomic Drag

The political justification for the universal tariff regime rested heavily on its theoretical capacity to generate vast sums of federal revenue to service the national debt. Conventional, static scoring models suggested that a sweeping tariff plan could raise over $5.2 trillion over a decade, with some estimates suggesting that a 15 percentage point increase in universal U.S. tariffs could generate $3.9 trillion before accounting for macroeconomic feedback loops.1 In nominal terms, the 2025 tariffs did raise an estimated $194.8 billion to $264 billion in new, inflation-adjusted customs revenue above the 2022–2024 historical averages.1

However, when analyzed through dynamic macroeconomic models—which account for behavioral shifts, the suppression of economic activity, and the erosion of broader tax bases—the revenue-generating capacity of the tariff regime is revealed to be a fiscal illusion. Tariffs function fundamentally as a massive negative supply shock to the domestic economy. By artificially inflating the cost of imported intermediate goods, machinery, and raw materials, tariffs increase the marginal cost of domestic investment and severely reduce the efficiency of resource allocation.1

The dynamic revenue estimates for the permanent Section 232 and temporary Section 122 tariffs indicate a yield of merely $517 billion from 2026 through 2035—substantially lower than the $662 billion projected by static, conventional estimates.2 Furthermore, the imposition of foreign retaliatory tariffs severely compounds this revenue loss. Incorporating the negative effects of imposed retaliatory countermeasures by trading partners further reduces the ten-year revenue yield by an additional $136 billion to $517 billion, depending on the severity of the retaliation.2 Attempting to resolve a $38.86 trillion sovereign debt crisis through a mechanism that dynamically yields less than $1 trillion over a decade is mathematically and structurally inefficient; it destroys a significant portion of the underlying economic wealth it is attempting to tax.1

| Economic Metric (10-Year Projection) | Static (Conventional) Estimate | Dynamic Estimate (Including Economic Drag) | Impact of Foreign Retaliation |

| Section 232 & 122 Revenue | $662 Billion | $517 Billion | Reduces revenue by an additional $136 Billion |

| 10% Universal Tariff Revenue | $2.2 Trillion | $1.7 Trillion | $1.4 Trillion |

| 15% Universal Tariff Revenue | $2.8 Trillion | $2.2 Trillion | $1.8 Trillion |

| 20% Universal Tariff Revenue | $3.4 Trillion | $2.6 Trillion | $2.0 Trillion |

Table 1: Static versus Dynamic Revenue Projections of U.S. Tariff Regimes (2026-2035).2

Incidence on the Domestic Household and Export Destruction

Beyond the failure to generate adequate sovereign debt relief, the incidence of the 2025-2026 tariff disruption was overwhelmingly borne by the domestic populace. Despite political rhetoric suggesting that foreign exporting nations absorb the duties, empirical analyses of millions of shipment records demonstrate that 90 to 96 percent of the tariff burden is passed directly through to U.S. importers and subsequently to the retail market.1

Consequently, imported personal consumption expenditures (PCE) for core goods and durable goods rose by 1.3 percent and 1.4 percent, respectively, directly tracking the implementation of the duties.3 This dynamic functions as a highly regressive domestic consumption tax. The Tax Foundation and Yale Budget Lab estimate that these tariffs impose an immediate, direct annual cost of between $600 and $1,000 on the average U.S. household, with previous, broader IEEPA tariffs costing households up to $2,800 annually.1 When compounding the effects of higher prices, depressed capital formation, and lower wages over a lifetime, macroeconomic models indicate that a middle-income American household faces staggering lifetime wealth destruction.1

Simultaneously, the geopolitical consequences of the tariff disruption triggered immediate and devastating retaliatory countermeasures. The European Union, Canada, Mexico, and China systematically targeted American agricultural and industrial exports.1 The Tax Foundation estimates that retaliatory tariffs of just 10 percent shrink U.S. GDP by 0.3 percent and result in the loss of 252,000 full-time equivalent jobs, while a 20 percent retaliatory scenario reduces the capital stock by 0.4 percent and destroys 460,000 jobs.7 In sum, the tariff approach deeply damaged the U.S. economy, impoverished American consumers, and fractured diplomatic alliances, all while generating suboptimal, economically destructive revenue for debt reduction.

The Allied Austerity Fallacy: Proportionality in Global Macroeconomics

Given the immense collateral damage, deadweight loss, and geopolitical alienation caused by the tariff regime, the theoretical proposition of a direct, non-repayable grant of $1 trillion annually for ten years, paid by the advanced allied economies to the United States, demands rigorous validation. Orthodox critiques of this model assert that draining $1 trillion annually from allied economies would invariably trigger draconian fiscal austerity, plunging the developed world into a severe, protracted recession and destroying global demand for U.S. exports.1

However, when this hypothesis is subjected to proportional macroeconomic analysis utilizing contemporary global GDP projections, the “allied austerity” argument reveals itself to be a gross overstatement. The capacity of the global economy to absorb a $1 trillion annual geopolitical security premium is immense, particularly when contrasted with the highly disruptive, deadweight costs of a universal tariff war.

Quantifying the Massive Scale of Global GDP Capacity

To accurately assess the feasibility of the capital transfer, it must be contextualized against the sheer scale of modern economic output. According to projections from the International Monetary Fund (IMF) and the World Bank for the year 2026, the global economy is valued at approximately $123.58 trillion in nominal terms.9 When adjusted for differences in the cost of living, the global economy measured by Purchasing Power Parity (PPP) reaches a staggering $219.22 trillion.10

The United States, as the world’s largest nominal economy, maintains a GDP of approximately $31.82 trillion.12 The allied economies capable of contributing to a global security stabilization grant possess immense collective fiscal capacity. The European Union’s nominal GDP is projected at $22.52 trillion in 2026, with a PPP valuation exceeding $30.18 trillion.11 The major advanced economies of the G7 (excluding the U.S.) represent tens of trillions in additional capacity, with Japan at $4.46 trillion, Germany at $5.33 trillion, the United Kingdom at $4.23 trillion, France at $3.56 trillion, Italy at $2.70 trillion, and Canada at $2.42 trillion.12

Furthermore, the Gulf Cooperation Council (GCC) and the broader Arab world represent a highly resilient, rapidly growing economic bloc. Buoyed by vast sovereign wealth reserves and the robust expansion of non-oil sectors—which now contribute over 75 percent of GDP in the United Arab Emirates and 71 percent in Saudi Arabia—the Arab world commands a nominal GDP approaching $4.50 trillion, with a PPP valuation of $18.87 trillion.14

| Economic Bloc / Nation | 2026 Projected Nominal GDP (USD) | 2026 Projected PPP GDP (Intl. $) | Share of Global PPP |

| Global Total | ~$123.58 Trillion | ~$219.22 Trillion | 100.0% |

| United States | $31.82 Trillion | $31.82 Trillion | 14.52% |

| European Union | $22.52 Trillion | $30.18 Trillion | 13.77% |

| China | $20.65 Trillion | $43.49 Trillion | 19.84% |

| Japan | $4.46 Trillion | $6.92 Trillion | 3.15% |

| India | $4.51 Trillion | $19.14 Trillion | 8.73% |

| Arab World (Including GCC) | ~$4.50 Trillion | $18.87 Trillion | 8.60% |

| Major Advanced Economies (G7) | $54.52 Trillion | $60.95 Trillion | 27.80% |

Table 2: Comprehensive Global Gross Domestic Product Projections for 2026 (Nominal vs. PPP).9

Contextualizing the $1 Trillion Levy as a Percentage of Output

If the hypothetical $1 trillion annual security grant were apportioned proportionally among the advanced allied economies—specifically the European Union, the United Kingdom, Japan, Canada, Australia, and the GCC states—the combined nominal GDP of this donor coalition exceeds $40 trillion. Mathematically, a $1 trillion annual contribution equates to approximately 2.5 percent of their collective nominal GDP.

Historically and contemporaneously, a capital reallocation of this magnitude is entirely feasible without inducing a severe macroeconomic depression. In response to the shifting geopolitical threat matrix following the 2022 invasion of Ukraine, NATO allies initiated sweeping commitments to increase core defense spending. The NATO Hague summit declaration of 2025 outlined aspirational targets of 5 percent of GDP for defense and security-related expenditures by 2035, including 3.5 percent for core defense.18 Between 2024 and 2030, Europe alone is projected to mobilize well over €1 trillion in additional defense acquisitions.20

The assertion that a $1 trillion collective contribution would plunge these economies into a protracted recession assumes that the grant must be funded entirely through immediate, highly contractionary domestic taxation. This assumption ignores the fundamental mechanics of sovereign finance. Governments routinely fund long-term geopolitical commitments and strategic investments through the issuance of sovereign debt, amortizing the cost over generations. Therefore, the macroeconomic “Paradox of Thrift” can be effectively circumvented if the allied security grant is financed through collective borrowing mechanisms rather than raw capital extraction.

In comparative terms, the hypothetical $1 trillion grant is a vastly superior, highly efficient mechanism for rectifying the U.S. fiscal imbalance. It represents a coordinated, predictable financial commitment that eliminates the massive deadweight loss, inflationary spikes, and retaliatory export destruction currently inflicted upon the global economy by the universal tariff regime. The true obstacle to the implementation of the grant is not the fiscal capacity of the allied economies, but rather the systemic disruption it poses to the global collateral architecture.

Deconstructing the Safe Asset Paradox and Shadow Banking Mechanics

If the $1 trillion allied grant is utilized by the U.S. Treasury to rapidly retire $10 trillion of outstanding sovereign debt over a decade, it introduces a severe structural hazard to the international financial architecture. This hazard, colloquially termed the “Safe Asset Paradox,” forms the core orthodox objection to aggressive U.S. debt consolidation.1 To architect creative solutions that bypass this hazard, one must first possess a highly nuanced understanding of the plumbing underlying global dollar liquidity and the indispensable role of safe assets.

The Indispensability of U.S. Treasuries as Global Collateral

U.S. Treasury securities are not merely instruments utilized to finance the deficit spending of the American government; they function as the foundational, risk-free collateral that underpins the entirety of the global financial system.1 Their supreme utility is derived from their unique characteristics: absolute safety (a near-zero probability of default), profound market liquidity, and “information-insensitivity”.23 Information-insensitivity dictates that because the payoffs of Treasuries are deemed riskless, they can be traded rapidly across borders “no questions asked,” eliminating the need for counterparties to conduct deep, time-consuming credit analyses.23

The clearest manifestation of global demand for these characteristics is the “convenience yield”—a nonpecuniary return that drives up the prices of safe assets and lowers their expected interest yields in equilibrium, simply because investors are willing to pay a premium for the safety and liquidity they provide.22

The most critical venue requiring this collateral is the repurchase agreement (repo) market. The repo market operates as a massive, collateralized short-term lending ecosystem where financial institutions (such as broker-dealers, hedge funds, and shadow banks) borrow cash overnight from entities with surplus capital (such as money market mutual funds), pledging safe assets as security.26 The scale of this market is staggering. According to data from the Office of Financial Research (OFR), the U.S. repo market averaged approximately $12.6 trillion in daily exposures in the third quarter of 2025.27 Of this $12.6 trillion, $4.4 trillion was centrally cleared by the Fixed Income Clearing Corporation, $3.1 trillion settled on tri-party platforms, and $5.0 trillion was transacted in the non-centrally cleared bilateral repo (NCCBR) market.27

The Collateral Multiplier and Systemic Fragility

Within the repo market and the broader shadow banking ecosystem, safe assets are subject to re-use or “rehypothecation.” A single U.S. Treasury bond can be pledged multiple times across different counterparties in a chain of transactions, a phenomenon quantified by the “collateral multiplier” or the velocity of collateral.28 Through Treasury re-use, financial intermediaries effectively multiply the safe asset benefits of a single bond to fulfill the global economy’s insatiable structural demand for secure stores of value.29

Consequently, if the United States abruptly receives $1 trillion annually and utilizes it to violently retire sovereign debt, the base layer of this collateral chain is aggressively contracted. A sharp reduction in the supply of U.S. Treasuries against highly inelastic global demand would trigger an acute scramble for safe assets. As supply vanishes, bond prices would skyrocket and yields would compress toward zero or turn negative, severely impairing the profitability and functioning of financial institutions.1

More dangerously, removing the underlying physical collateral from the repo market causes the collateral multiplier to collapse. Without sufficient Treasuries to pledge, overnight lending seizes up, abruptly freezing global liquidity. Historical precedent demonstrates that when true sovereign safe assets are structurally scarce, the shadow banking sector attempts to satisfy demand by manufacturing “synthetic” safe assets. Institutions pool inherently risky loans (such as subprime mortgages, auto loans, or lower-grade corporate debt) and tranche them through financial engineering to create AAA-rated instruments.1 When the market inevitably recognizes the latent risk and information-sensitivity in these synthetic assets, panic ensues, resulting in fire sales, collateral haircuts, and systemic contagion reminiscent of the 2008 Global Financial Crisis.1

Therefore, the central obstacle to implementing the $1 trillion allied grant is the preservation of the global collateral base. If the U.S. debt is to be successfully consolidated, new architectural solutions must be engineered to either replace the withdrawn U.S. Treasuries with equivalent, high-quality global collateral, or to decouple the servicing of the debt from the physical retirement of the bonds.

Creative Paradigm I: Mutualized Issuance of “Allied Security Bonds”

The most direct and economically elegant solution to the Safe Asset Paradox aligns with the proposition to “issue new bonds for the repayment of America.” To execute the $1 trillion annual grant without triggering a global collateral shortage, the contributing allied nations must fund their geopolitical dues not through contractionary domestic austerity, but through the coordinated issuance of mutualized, highly rated sovereign debt.

Architecting the Eurobond and Allied Equivalents

The European Union currently possesses the nascent institutional architecture required to generate a massive new supply of safe assets. Following the precedents set by the NextGenerationEU recovery instrument, and the integration necessitated by the ongoing energy and security crises on the continent, there is significant macroeconomic momentum for the creation of a deep and liquid “Eurobond” market.20 Historically, the European debate on safe assets has oscillated between proposals for “synthetic” safe assets (such as Sovereign Bond-Backed Securities) and genuine, jointly issued mutualized debt, often referred to conceptually as “Blue Bonds”.30

If the European Union, acting in concert with major partners such as the United Kingdom, Japan, Canada, Australia, and the capital-rich GCC states, were to pool their sovereign creditworthiness, they could issue a unified, AAA-rated debt instrument: the Allied Security Bond.

The mechanics of this capital transfer would operate as a perfect macroeconomic offset:

- Issuance: The allied coalition jointly issues $1 trillion in Allied Security Bonds annually to global capital markets.

- Transfer: The $1 trillion in cash liquidity raised from the bond sale is transferred directly to the U.S. Treasury as the non-repayable hegemonic security grant.

- Retirement: The U.S. Treasury utilizes the influx of cash to buy back and permanently retire $1 trillion of outstanding U.S. sovereign debt.

Preserving Repo Market Equilibrium and Global Liquidity

From the perspective of global shadow banking, Basel III regulatory requirements, and the repo market, the net supply of global safe assets remains entirely unchanged. For every $1 of U.S. Treasury collateral withdrawn from the financial system by the U.S. government, $1 of AAA-rated Allied Security Bond collateral is simultaneously injected into the system by the allied coalition.

Empirical research conducted by the Bank for International Settlements (BIS) on international portfolio choice and safe asset substitutability confirms the viability of this mechanism. In global bond markets, safe assets face highly inelastic demand from investment funds. When the supply or return of U.S. Treasuries fluctuates, funds naturally substitute them with other high-quality global bonds to maintain portfolio stability.35 A well-designed, highly liquid Allied Security Bond, backed by the taxation authority or sovereign wealth of the combined Western and Pacific alliance, would effectively assume the mantle of global collateral. It would anchor bilateral and tri-party repo markets, fulfill the High-Quality Liquid Asset (HQLA) requirements of the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) under Basel III, and provide a stable store of value for global central banks.36

This paradigm achieves profound dual objectives. First, it provides the United States with genuine, non-inflationary debt relief. By shrinking the supply of U.S. Treasuries, the U.S. government lowers its own domestic borrowing costs, stabilizing the fiscal trajectory and preserving the purchasing power of the American consumer without relying on the destructive friction of tariffs. Second, it catalyzes the maturation of the European and allied capital markets, fostering deep financial integration and establishing a multipolar safe asset framework that permanently insulates the global economy from unilateral U.S. fiscal shocks.36

Creative Paradigm II: The Sovereign Wealth “Endowment Sterilization” Model

An alternative, highly creative approach to resolving the U.S. debt crisis via the allied grant involves fundamentally rethinking the definition of “debt reduction.” Rather than utilizing the $1 trillion annual transfer to physically buy back and retire existing U.S. Treasuries—which directly precipitates the collateral shortage—the U.S. government could utilize the grant to capitalize a massive, state-owned investment vehicle.

Capitalizing a United States Sovereign Wealth Fund

In early 2026, the U.S. administration issued Executive Order 14196, directing the Secretary of the Treasury and the Secretary of Commerce to develop a comprehensive blueprint for the establishment of a United States Sovereign Wealth Fund (SWF).40 The stated aims of this initiative include promoting long-term fiscal sustainability, establishing economic security for future generations, and maximizing the stewardship of national wealth.40 Historically, the world’s largest sovereign wealth funds are capitalized by massive structural current account surpluses or commodity export windfalls, as seen in the GCC states or Norway’s Government Pension Fund Global. The United States, which runs persistent trade and fiscal deficits, severely lacks these organic, domestic funding streams.41

The hypothetical $1 trillion annual allied security grant provides the perfect, non-inflationary capitalization mechanism for a U.S. SWF.

Under the “Endowment Sterilization Model,” the U.S. Treasury would continue to roll over its existing $38.86 trillion in gross national debt. It would not retire the principal. Therefore, the total supply of U.S. Treasuries available to the global repo market and the shadow banking sector remains intact, completely bypassing the Safe Asset Paradox and ensuring that global dollar liquidity remains highly functional. The incoming $1 trillion annual grant would instead be deposited entirely into the newly established U.S. Sovereign Wealth Fund.

The Mechanics of Yield Generation and Debt Servicing

The U.S. SWF, managed by an independent, highly regulated board with a strict fiduciary mandate—insulated from domestic political capture and short-term electoral cycles—would invest the $1 trillion annual influx into a globally diversified, return-seeking portfolio.41 This portfolio would encompass global equities, international infrastructure projects, strategic critical mineral supply chains, and high-yield emerging market sovereign and corporate bonds.41

Assuming a conservative, long-term annualized real return of 5 to 7 percent, a U.S. SWF capitalized with $10 trillion in allied grants over a decade would generate a massive internal endowment, yielding between $500 billion and $700 billion in annual passive income. These capital gains, dividends, and interest yields would be swept directly into the U.S. Treasury’s general fund, specifically earmarked by statute to service the net interest payments on the national debt.

Currently, the U.S. spends over $1 trillion annually on debt service, a paralyzing burden that consumes nearly 19 percent of all federal revenue and severely crowds out discretionary spending, infrastructure investment, and military readiness.1 By generating hundreds of billions in external, compounding yield through the SWF, the United States essentially sterilizes its debt burden. The gross national debt remains on the balance sheet, ensuring the global financial system retains its indispensable U.S. Treasury collateral, but the agonizing fiscal cost of carrying that debt is shifted entirely onto the returns generated by allied capital transfers. This innovative solution perfectly navigates the systemic hazards of debt reduction by decoupling the fiscal cost of the debt from the physical existence of the debt in global capital markets.

Creative Paradigm III: Modernizing the IMF Substitution Account

Should the issuance of mutualized Allied Security Bonds prove politically untenable due to European fiscal fragmentation, and should the creation of a massive U.S. Sovereign Wealth Fund present unacceptable domestic governance risks, the international community must look to supranational monetary architecture. The resolution to the safe asset shortage and the execution of the allied grant can be effectively facilitated by resurrecting and modernizing the International Monetary Fund (IMF) Substitution Account.

Historical Precedent and the Triffin Dilemma

The concept of a Substitution Account is a persistent phenomenon in international monetary history. In the late 1970s, facing a crisis of confidence in the U.S. dollar and extreme exchange rate volatility following the collapse of the Bretton Woods system, the management of the IMF proposed a mechanism whereby foreign central banks could deposit their surplus U.S. dollar reserves into a specialized IMF account.46 In exchange for depositing these dollars, the central banks would receive claims denominated in Special Drawing Rights (SDRs)—the IMF’s quasi-currency and unit of account, the value of which is based on a weighted basket of major global currencies (currently the U.S. dollar, euro, Chinese renminbi, Japanese yen, and British pound).47

The original proposal ultimately foundered in the early 1980s primarily because potential users insisted that the United States take sole responsibility for maintaining the SDR value of the dollars deposited in the account—a currency risk requirement the U.S. Treasury summarily rejected.48 The proposal lay dormant until it was briefly revived in 2009 by the Governor of the People’s Bank of China amidst the fallout of the Global Financial Crisis.48 However, in the context of the contemporary $38.86 trillion U.S. debt crisis and the willingness of allies to provide a $1 trillion annual grant, a modernized Substitution Account provides an unparalleled avenue for global financial restructuring.

The Hegemonic Stability Account and SDR Expansion

To operationalize the grant without destroying market liquidity, the IMF would establish a modernized “Hegemonic Stability Account.” The allied nations (the EU, Japan, the GCC, etc.) would fund their $1 trillion annual geopolitical commitment by transferring a portion of their existing U.S. Treasury holdings, or newly acquired U.S. dollars, directly into this specialized IMF account.

- Sterilization and Debt Relief: Once the U.S. Treasuries are deposited into the Hegemonic Stability Account, they are effectively quarantined from the open market. This immediately reduces the U.S. government’s exposure to foreign sovereign rollover risk and market volatility. The IMF, acting as the custodian, could then negotiate a bilateral treaty with the U.S. Treasury to slowly convert these quarantined bonds into perpetual, non-marketable zero-coupon bonds. This provides the United States with absolute, immediate relief from both principal repayment and compounding interest costs.

- SDR Issuance: In exchange for their massive contributions to the account, the allied nations receive highly liquid, SDR-denominated reserve claims. Because the SDR is backed by a basket of currencies, exchange rate risk is diversified, providing allied central banks with a highly stable store of value.52

- Private Sector Integration: The most critical modification to the historical proposal involves integrating the shadow banking sector. To prevent a collateral shortage in private markets, the IMF would need to take the unprecedented step of allowing approved private financial institutions—beyond just central banks and prescribed multilateral holders—to hold and utilize SDR-denominated claims. If these SDR claims are legally recognized as High-Quality Liquid Assets (HQLA) in the repo market, they seamlessly replace the quarantined U.S. Treasuries as the bedrock of global collateral.

By utilizing the IMF as a supranational clearinghouse, the global economy systematically transitions away from an asymmetric reliance on U.S. domestic debt toward a multilateral, basket-backed safe asset. This addresses the long-standing structural vulnerability of the global financial system—solving the modern iteration of the Triffin Dilemma—while allowing the U.S. to rapidly and safely deleverage its balance sheet.51

Creative Paradigm IV: Sovereign Debt Restructuring Mechanisms

Beyond the creation of entirely new asset classes or supranational accounts, creative financial engineering applied directly at the contract level of U.S. sovereign debt can significantly alleviate the fiscal burden without triggering systemic collapse. The sovereign debt restructuring literature, typically reserved for emerging market crises, offers several highly effective mechanisms that can be adapted for the world’s largest advanced economy.54

The Century Bond and Consol Conversion

Rather than relying on allied nations to provide raw cash grants that disrupt market equilibrium, the U.S. Treasury could initiate a massive, voluntary debt-swap program directed specifically at allied central banks. Allied nations currently hold trillions of dollars in U.S. Treasuries as foreign exchange reserves.38 Under a coordinated diplomatic initiative—representing their contribution to global security and the $1 trillion annual mandate—these allies could agree to exchange their short- and medium-term U.S. Treasuries for “Century Bonds” (100-year maturity) or “Consols” (perpetual bonds with no maturity date).

By extending the maturity profile of a significant tranche of the national debt into perpetuity, the U.S. Treasury effectively eliminates the principal repayment risk. If these perpetual bonds are intentionally issued with heavily subsidized, below-market interest rates—the interest differential representing the actual “security grant” concession from the allies—the U.S. drastically lowers its annual net interest expense. Crucially, because these perpetual bonds remain active on the balance sheet and can still be traded or pledged, they continue to function as viable collateral within the global financial system, thereby entirely circumventing the Safe Asset Paradox.

Incorporating Geopolitical “Pause Clauses”

Drawing inspiration from recent innovations in sovereign debt instruments, such as the Inter-American Development Bank’s (IDB) Principal Payment Option (PPO)—which allows nations to suspend debt service in the aftermath of severe climate disasters—the United States could pioneer the use of geopolitical “Pause Clauses”.56

Newly issued U.S. Treasuries absorbed by allied central banks could include contractual stipulations allowing the U.S. government to unilaterally suspend interest and principal payments for a period of up to three years in the event of a major, mutually defined geopolitical crisis (e.g., a defense of Taiwan, or a major Article 5 engagement in Eastern Europe).56 By accepting bonds with these specific clauses, allied investors explicitly subsidize U.S. military mobilization. This mechanism elegantly shifts the financial risk of global security enforcement directly onto the bondholders, providing the United States with immediate, localized fiscal flexibility precisely when it is required to act as the arsenal of democracy, without necessitating a permanent contraction of the global safe asset supply.

Conclusion

The resolution of the $38.86 trillion U.S. sovereign debt crisis remains the defining macroeconomic and geopolitical challenge of the decade. The unilateral attempt to deleverage this paralyzing burden through a punitive, universal tariff regime has proven to be an empirical and structural failure. Tariffs represent a highly inefficient mechanism for sovereign debt consolidation; they function as a massive negative supply shock, inflicting severe deadweight loss, driving domestic inflation, and actively shrinking the U.S. economic output they intend to tax, while provoking retaliatory measures that devastate export markets.

The theoretical proposition of a $1 trillion annual security grant provided by a coalition of allied nations offers a mathematically superior, non-inflationary alternative for the American domestic economy. The orthodox critique of this grant—that extracting such capital would require impossible levels of global austerity—is fundamentally unfounded when contextualized against a massive global PPP GDP of $219.22 trillion and the immense, resilient capacity of the European Union, the G7, and the Gulf Cooperation Council. A $1 trillion annual contribution equates to a highly manageable percentage of allied output, easily financed through collective borrowing rather than contractionary taxation.

The true impediment to the grant is structural: the rapid retirement of $10 trillion in U.S. Treasury debt would destroy the collateral foundation of the global repo market and the shadow banking system, risking a catastrophic liquidity freeze and a severe safe asset shortage.

However, as this exhaustive analysis demonstrates, the Safe Asset Paradox is not an insurmountable barrier; it is an engineering challenge that can be overcome through creative financial architecture. By looking beyond the fixed, unipolar constraints of the current international monetary system, highly effective, multipolar solutions can be operationalized. Whether through the mutualized issuance of AAA-rated Allied Security Bonds to seamlessly replace withdrawn Treasuries, the capitalization of a U.S. Sovereign Wealth Fund to generate debt-servicing yield without retiring principal, the modernization of the IMF Substitution Account to transition global reserves into SDRs, or the deployment of perpetual debt swaps and geopolitical pause clauses, the mechanisms exist to execute a massive geopolitical capital transfer safely. The sustainable consolidation of U.S. sovereign debt will not be achieved through the destructive friction of isolationist trade walls, but through a calibrated, cooperative, and architecturally innovative reconfiguration of the global financial system.

Works cited

- Macroeconomic and Geopolitical Evaluation of U.S. Sovereign Debt Consolidation_ Universal Tariffs Versus a Hypothetical Allied 1 Trillion annual Security Grant – Hans Smedema Affair.pdf

- Tracking the Impact of the Trump Tariffs & Trade War – Tax Foundation, accessed March 29, 2026, https://taxfoundation.org/research/all/federal/trump-tariffs-trade-war/

- Tracking the Economic Effects of Tariffs | The Budget Lab at Yale, accessed March 29, 2026, https://budgetlab.yale.edu/research/tracking-economic-effects-tariffs

- Working Paper 25-19: Tariffs as fiscal policy – Peterson Institute for International Economics, accessed March 29, 2026, https://www.piie.com/sites/default/files/2025-09/wp25-19.pdf

- The US revenue implications of President Trump’s 2025 tariffs | PIIE, accessed March 29, 2026, https://www.piie.com/publications/piie-briefings/2025/us-revenue-implications-president-trumps-2025-tariffs

- Tariffs in 2025: Short-run impacts on the US economy – Brookings Institution, accessed March 29, 2026, https://www.brookings.edu/articles/tariffs-in-2025-short-run-impacts-on-the-us-economy/

- How Much Revenue Can Tariffs Really Raise for the Federal Government? – Tax Foundation, accessed March 29, 2026, https://taxfoundation.org/research/all/federal/universal-tariff-revenue-estimates/

- Who Is Paying for the 2025 U.S. Tariffs? – Liberty Street Economics, accessed March 29, 2026, https://libertystreeteconomics.newyorkfed.org/2026/02/who-is-paying-for-the-2025-u-s-tariffs/

- World Economic Outlook (October 2025) – GDP, current prices – International Monetary Fund, accessed March 29, 2026, https://www.imf.org/external/datamapper/NGDPD@WEO/OEMDC/ADVEC/WEOWORLD

- The Entire Global Economy in 2026 in One Chart (GDP, PPP) – Visual Capitalist, accessed March 29, 2026, https://www.visualcapitalist.com/the-global-economy-by-ppp-2026/

- World Economic Outlook (October 2025) – GDP, current prices – International Monetary Fund, accessed March 29, 2026, https://www.imf.org/external/datamapper/PPPGDP@WEO/OEMDC/ADVEC/WEOWORLD

- GDP by Country (2026) – IMF – Worldometer, accessed March 29, 2026, https://www.worldometers.info/gdp/gdp-by-country/?source=imf&year=2026&metric=nominal®ion=worldwide

- European Union – IMF DataMapper, accessed March 29, 2026, https://www.imf.org/external/datamapper/profile/EU

- GCC Corporate And Infrastructure Outlook 2026: Stability Despite Uncertainty – S&P Global, accessed March 29, 2026, https://www.spglobal.com/ratings/en/regulatory/article/gcc-corporate-and-infrastructure-outlook-2026-stability-despite-uncertainty-s101666045

- GDP per capita, PPP (current international $) – World Bank Open Data, accessed March 29, 2026, https://data.worldbank.org/indicator/NY.GDP.PCAP.PP.CD

- World Economic Outlook (October 2025) – GDP per capita, current prices, accessed March 29, 2026, https://www.imf.org/external/datamapper/PPPPC@WEO/SAU/QAT/KWT/ARE/BHR

- World Economic Outlook (October 2025) – GDP based on PPP, share of world, accessed March 29, 2026, https://www.imf.org/external/datamapper/PPPSH@WEO/OEMDC/ADVEC/WEOWORLD

- Macroeconomic impacts of defense spending | Global Excellence Chronicle Magazine, accessed March 29, 2026, https://gecmagz.com/macroeconomic-impacts-of-defense-spending/

- Key Challenges Facing Europe’s Proposed Defense Expansion – Oliver Wyman, accessed March 29, 2026, https://www.oliverwyman.com/our-expertise/insights/2025/aug/key-challenges-facing-europe-proposed-defense-expansion.html

- Europe’s €1 trillion challenge for flexibility and scale – McKinsey, accessed March 29, 2026, https://www.mckinsey.com/industries/aerospace-and-defense/our-insights/europes-1-trillion-euros-challenge-for-flexibility-and-scale

- The great repricing: Are US Treasuries still a safe haven? – State Street, accessed March 29, 2026, https://www.statestreet.com/us/en/insights/the-great-repricing-us-treasuries

- Are US Treasury Bonds Still a Safe Haven? – NBER, accessed March 29, 2026, https://www.nber.org/reporter/2020number3/are-us-treasury-bonds-still-safe-haven

- Fragility of Safe Asset Markets – Office of Financial Research (OFR), accessed March 29, 2026, https://www.financialresearch.gov/working-papers/files/OFRwp-23-02_fragility-of-safe-asset-markets.pdf

- The Safe Assets Shortage Conundrum, accessed March 29, 2026, https://www.sfu.ca/~kkasa/Caballero_Farhi-Gourinchas_JEP17.pdf

- Preserving the global safe asset status of US Treasuries and the US dollar is in everyone’s interest | PIIE, accessed March 29, 2026, https://www.piie.com/blogs/realtime-economics/2025/preserving-global-safe-asset-status-us-treasuries-and-us-dollar

- What is the repo market, and why does it matter? – Brookings Institution, accessed March 29, 2026, https://www.brookings.edu/articles/what-is-the-repo-market-and-why-does-it-matter/

- Sizing the U.S. Repo Market | Office of Financial Research, accessed March 29, 2026, https://www.financialresearch.gov/the-ofr-blog/2025/12/04/sizing-us-repo-market/

- Shadow Banks and the Collateral Multiplier – UMass ScholarWorks, accessed March 29, 2026, https://scholarworks.umass.edu/bitstreams/636519f5-b99a-4170-b4ed-f58d10770285/download

- What Drives U.S. Treasury Re-use? – Federal Reserve, accessed March 29, 2026, https://www.federalreserve.gov/econres/feds/files/2020103r1pap.pdf

- The Handbook of Global Shadow Banking, Volume II: The Future of Economic and Regulatory Dynamics [1st ed.] 9783030348168, 9783030348175 – DOKUMEN.PUB, accessed March 29, 2026, https://dokumen.pub/the-handbook-of-global-shadow-banking-volume-ii-the-future-of-economic-and-regulatory-dynamics-1st-ed-9783030348168-9783030348175.html

- This Time Was Different: The Global Safe Asset Shortage and Shadow Banking in Socio-Historical Perspective – EconStor, accessed March 29, 2026, https://www.econstor.eu/bitstream/10419/251255/1/CITYPERC-WPS-2020-01.pdf

- Financial stability risks from basis trades in the US Treasury and euro area government bond markets – European Central Bank, accessed March 29, 2026, https://www.ecb.europa.eu/press/financial-stability-publications/fsr/focus/2024/html/ecb.fsrbox202405_03~09cad3d18d.en.html

- Could “Eurobonds” Replace US Treasuries? – YouTube, accessed March 29, 2026, https://www.youtube.com/watch?v=nGQYm6gM2ks

- No free lunch: what it takes to build Europe’s safe asset – OMFIF, accessed March 29, 2026, https://www.omfif.org/2025/06/no-free-lunch-what-it-takes-to-build-europes-safe-asset/

- Global or regional safe assets: Evidence from bond substitution patterns, accessed March 29, 2026, https://www.bis.org/publ/work1254.htm

- How could a common safe asset contribute to financial stability and financial integration in the banking union? – European Central Bank, accessed March 29, 2026, https://www.ecb.europa.eu/press/fie/article/html/ecb.fieart202003_02~2b34819f75.en.html

- Commission proposes maintaining current liquidity rules to strengthen EU financial markets, accessed March 29, 2026, https://finance.ec.europa.eu/news/commission-proposes-maintaining-current-liquidity-rules-strengthen-eu-financial-markets-2025-03-31_en

- The search for safe assets – Atlantic Council, accessed March 29, 2026, https://www.atlanticcouncil.org/blogs/econographics/the-search-for-safe-assets/

- A Proposal to Create a European Safe Asset – Levy Economics Institute of Bard College, accessed March 29, 2026, https://www.levyinstitute.org/wp-content/uploads/2024/02/pn_19_1.pdf

- A United States Sovereign Wealth Fund: First Impressions | Insights | Greenberg Traurig LLP, accessed March 29, 2026, https://www.gtlaw.com/en/insights/2025/2/a-united-states-sovereign-wealth-fund-first-impressions

- A US sovereign wealth fund? A confused solution to an undefined problem | PIIE, accessed March 29, 2026, https://www.piie.com/blogs/realtime-economics/2025/us-sovereign-wealth-fund-confused-solution-undefined-problem

- Why the US Trade Deficit Persists – Fair Observer, accessed March 29, 2026, https://www.fairobserver.com/economics/why-the-us-trade-deficit-persists/

- 360° View of a US Sovereign Wealth Fund | Wilson Center, accessed March 29, 2026, https://www.wilsoncenter.org/article/360deg-view-us-sovereign-wealth-fund

- Global Bond Managers Seek to Widen Safe Asset Menu – Andersen Institute, accessed March 29, 2026, https://anderseninstitute.org/the-quiet-repricing-of-u-s-treasuries-in-a-fragmenting-world/

- Why the National Debt Matters for National Security – Bipartisan Policy Center, accessed March 29, 2026, https://bipartisanpolicy.org/explainer/why-the-national-debt-matters-for-national-security/

- 3 Substitution in the International Monetary System in – IMF eLibrary, accessed March 29, 2026, https://www.elibrary.imf.org/display/book/9780939934133/ch003.xml

- A Substitution Account: Precedents and Issues – Federal Reserve Bank of New York, accessed March 29, 2026, https://www.newyorkfed.org/medialibrary/media/research/quarterly_review/1979v4/v4n2article8.pdf

- Renovation of the Global Reserve Regime: Concepts and Proposals by Peter B. Kenen, Princeton University CEPS Working Paper No., accessed March 29, 2026, https://gceps.princeton.edu/wp-content/uploads/2017/01/208kenen.pdf

- 2025 External Sector Report: Global Imbalances in a Shifting World – International Monetary Fund, accessed March 29, 2026, https://www.imf.org/-/media/files/publications/esr/2025/english/text.pdf

- What is the SDR? – International Monetary Fund, accessed March 29, 2026, https://www.imf.org/en/About/Factsheets/Sheets/2023/special-drawing-rights-sdr

- Reforming the Global Reserve Regime: The Role of a Substitution Account – RePEc, accessed March 29, 2026, https://ideas.repec.org/a/bla/intfin/v13y2010i1p1-23.html

- Official Reserve Asset Choice and Substitution Account Proposals, accessed March 29, 2026, https://www.dallasfed.org/~/media/documents/research/papers/1980/wp8002.pdf

- Reforming the Global Reserve System – IMF eLibrary, accessed March 29, 2026, https://www.elibrary.imf.org/downloadpdf/display/book/9781513514277/ch014.pdf

- The 2020-2025 Sovereign Debt Crisis: What have we learnt and what lies ahead? | Lazard, accessed March 29, 2026, https://www.lazard.com/research-insights/the-2020-2025-sovereign-debt-crisis-what-have-we-learnt-and-what-lies-ahead

- Sovereign Debt Restructuring: – IADB Publications, accessed March 29, 2026, https://publications.iadb.org/publications/english/document/Sovereign-Debt-Restructuring-The-Need-for-a-New-Approach.pdf

- INNOVATIONS IN SOVEREIGN DEBT: TAKING DEBT PAUSE CLAUSES TO SCALE – Centre for Disaster Protection, accessed March 29, 2026, https://www.disasterprotection.org/s/230406_Innovations-in-Sovereign-Debt-Taking-Pause-Clauses-to-Scale_FINAL.pdf